Join the campaign fun now!

Why a Forensic Audit?

Some might ask "if we did an Efficiency Audit in 2023, why do we need a Forensic Audit in 2026?" Let's cut through the confusion together by asking some questions we might all like answers to. Have you ever wondered why our school budgets never seem to be enough? How no matter how much financial assistance or what form it comes in the grants, funds or bonds from the state, federal government, and the tax payers just never seems to cover the needs of the school district? Well as a school board member and a parent in this district I have come across some things that simply aren't adding up. I don't mean figuratively- I mean literally, are not adding up. So, the real question is who in the heck wouldn't want a deep dive into how our tax dollars are used to best educate our students and keep them safe? What our slate has determined is that we need to understand at a deep level how these funds are being applied. Right now, it is difficult to understand how the district uses this much money and our student outcomes are barely improving. We are again facing a deficit budget while battling a shrinking student enrollment (we are down almost 2,000 kids this school year) and have had no success in closing the literacy gap in our most vulnerable student groups.

The administration and some board colleagues say we have done an efficiency audit already- and we have our answers and there is nothing more to see here. Is that true? What do we know so far- and is there more we might need to understand before we cut the budget or ask for a bond? You tell me…

Shallow Dives, Deep Doubts

Does reading the auditors introductory letter give you confidence on the depth of the audit? The introductory letter clearly states that:

“We were engaged to… perform this agreed-upon procedures engagement…we were not engaged to and did not conduct an examination or review, the objective of which would be the expression of an opinion or conclusion…on the specified procedures above. Accordingly, we do not express such an opinion or conclusion. Had we performed additional procedures other matters might have come to our attention that would have been reported to you.”

So, Weaver is telling us PLAINLY that this was a surface report- they didn’t dig deep because the scope created by the administration was too narrow to yield deeper analysis. WOW!

Deaf Ears, Diminished Trust

The community has LOTS of questions about how CFISD spends money- both big picture and nitty gritty questions. State legislators do too - our pleas to address the Local Optional Homestead Exemption (LOHE) over many visits to Austin fell on deaf ears. State Representatives and Senators pushed back on our spending. The “efficiency audit” did not provide any depth to answer these critical questions and concerns. We must be able to answer if we are going to successfully argue for LOHE relief in Austin- or have the boldness to bring a bond referendum before our voters. We need an in-depth forensic audit to understand the “state of Denmark”- and make sure that “nothing is rotten in the state of Denmark.” This is how we instill trust in our community.

Spending More, Learning Less?

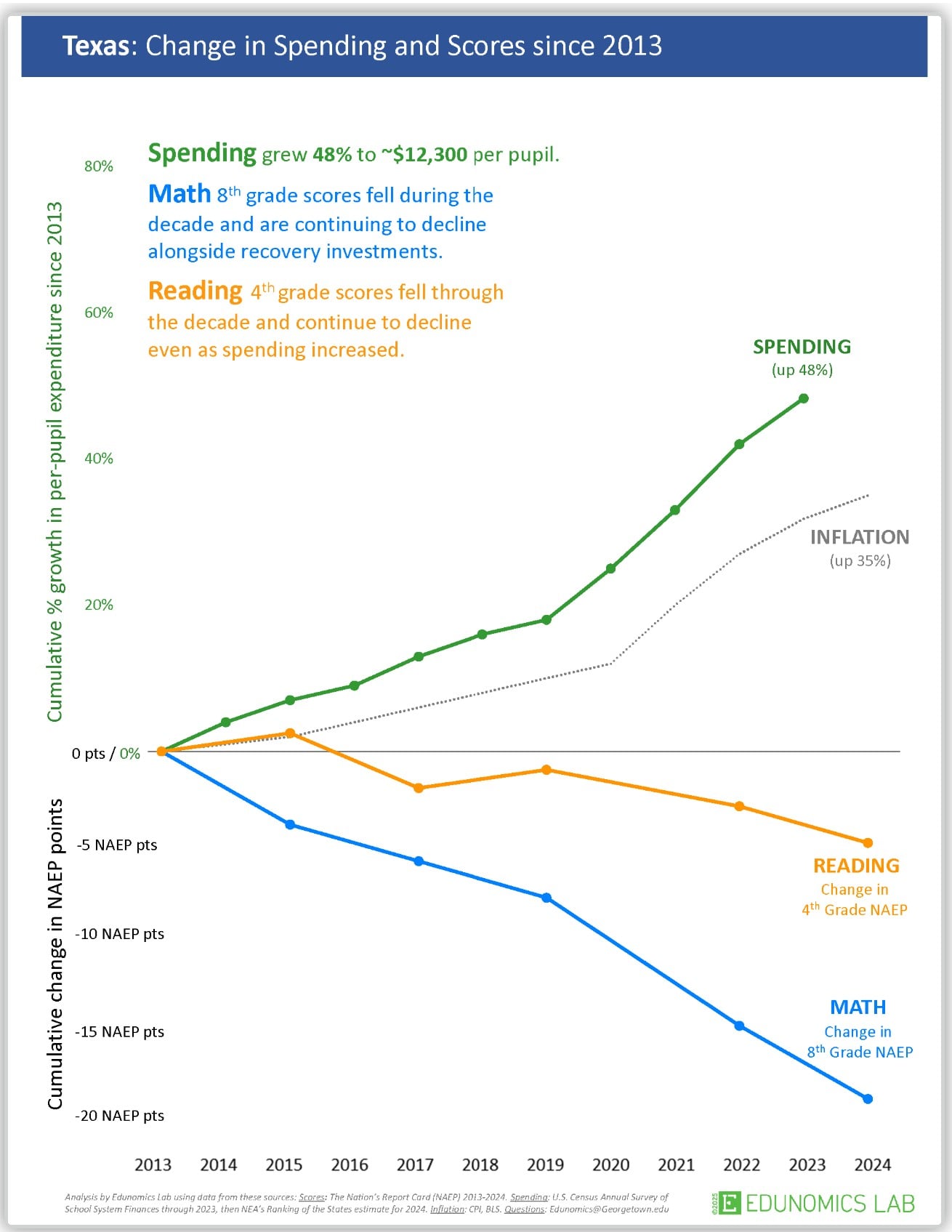

Big picture, many people reached out to me when NAEP data came out. CFISD had some campuses that were selected for participation in the national exam to measure educational progress in our nation. This 2024 data from Edunomics Lab shows the ROI in Texas of the change in spending alongside reading and math outcomes. This picture is not pretty! Spending outpaced inflation, while 8th grade math and 4th grade reading scores fell. Leaders are asking the question - how are you spending the money in education if it’s not improving reading and writing?

The Accountability Gap

You may feel a statewide example is too global, fair point, so let’s get local. Some smart taxpayers sent me this spreadsheet of “CFISD Actuals” that they created using TEA data over the period 2019-2024. They believe we are spending more than we should, evidenced by a huge deficit budget, and sought to understand our spending. Truth is their “local yokel” report tells us more about our spending than the Weaver Efficiency Audit.

According to their calculations, while we had a 2% rate of growth in student enrollment and the cumulative inflation rate was 19.81%, operational expenditures went up 30%. Why did the following functions have such large increases in spending? Let’s find it in the Efficiency Audit - oh, we can’t. Why do we have to count on the citizens of our district to provide this 5-year perspective?

|

TEA Data Line Item |

% Increased By |

$ Increased By |

|---|---|---|

|

Supplies & Materials (Object 62xx) |

69% |

$48.4M |

|

Curriculum & Staff Development (Function 13) |

48% |

$11.2M |

|

Guidance Counseling Services (Function 31) |

58% |

$23.3M |

|

Transportation (Function 34) |

3% |

$2.1M |

|

Students with Disabilities (PICs 23, 33, 43) |

53% |

$66.8M |

|

Career & Technical (PIC 22) |

43% |

$13.0M |

|

Un-allocated (PIC 99) Note: $333M Line Item |

24% |

$69.1M |

These are just a sampling of huge increases in spending - and I added data about transportation to make a point. What do we choose to cut and why? This raises so many, many questions for me! Why such large increases? What is this “Un-allocated” category for $333M. I think you are maybe understanding why a forensic audit is needed! There is a lot to be explored and queried. All things need to be placed in the light.

Questions Invite Contempt

Then, we should always be in the practice of asking questions to rule out corruption. I will get started here - but another article will have to follow. What happens when someone starts asking questions about contracts and possible corruption? You guessed it - the parties under pressure start accusing them of corruption! I have been asking:

- What were the conditions under which all of the budget functions line above were spent?

- What contracts were issued and paid from the debt service expenditures of $1,257,000,000 between 2019-2024?

- Who did all of those dollars for architectural services and construction go to?

- How many companies got contracts from the $3.3B we still owe today in Bond principal? How was it decided?

- How many of these companies donated to sitting board members’ election campaigns before they voted on the contracts?

- What did the competitive pricing landscape look like - did the regional pricing structure for building schools outpace other construction of other genres of buildings over the same time period?

- What subcontractors did construction companies use? Could we audit the subs to learn who supplied them raw materials or was this excluded in our CFISD contracts? Is this standard to exclude?

Did we get insight into these long-term, deep, ethical financial questions in the Weaver construction audit we were provided to leave a “clean trail” as the board was about to turn over in September 2023? You tell me…

Ahhh… it appears once again Weaver has some qualifying language in the scope of their audit report:

“Our scope did not include evaluating the District’s compliance with the Texas Government Code §2254.004, Contracting for professional services of architect, engineer, or surveyor.”

Well… I am still waiting for answers. Maybe we need a forensic audit of the bond program and contracts to find out the answers to these burning questions? What about for other materials and supplies, what continuing contracts were in place over the last 4-year period? Were there millions of dollars in expenditures that were not spent for the children’s benefit? How can we know? A forensic audit- one with the level of sophistication to even query computer records to verify that no changes have been made to any records in preparation for the audit.

Financial Truth Builds Trust

Look, we have to stand clean before God and everybody with financial questions answered about the kind of stewards we are of tax-payer money. We must be able to answer in confident detail if we are going to successfully argue for LOHE relief in Austin, balance our budget while making sure student achievement does not suffer, or have the boldness to bring a bond referendum before our voters. We need an in-depth forensic audit to understand the “state of Denmark”- and make sure that “nothing is rotten in the state of Denmark.” This is how we instill trust in our supportive community.

Investing in Financial Accountability

So, what is a forensic audit? A forensic audit in a school district is an in-depth examination of financial records, internal controls, and procedures designed to detect fraud, identify noncompliance, strengthen transparency, and evaluate governance practices. The process is far more intensive than a standard audit, focusing on uncovering potential misconduct, mismanagement, or misuse of funds through detailed investigation and evidence gathering.

See button below, page 14, of this example of even a simple depth of analysis of expenditures and accounting that is flagrantly missing from the report we commissioned.

The audit will cost us money, maybe even $200,000 - $400,000, given the size and complexity of the district, the audit scope, quality and organization of financial records, suspected fraud or irregularities, and the level of staff cooperation. The experience of the audit firm and the timing of the audit engagement will also play a role. However, it will all be worth it. We need to KNOW the state of our financial house so that we can proceed confidently as we exercise our fiduciary responsibility as trustees.

I return to where I started… who WOULDN’T want a forensic audit? And if so, why not? Make it make sense.